Tunisia as a Mediterranean Healthcare Hub

1. Introduction: Tunisia as a Mediterranean Healthcare Hub

Tunisia has solidified its position as the preeminent healthcare gateway for the Maghreb and Mediterranean regions. This "Medical Renaissance" is not a product of chance, but a strategic alignment where the private medical tourism industry acts as a high-octane fuel for the nation’s broader health infrastructure. Far from being a mere export of services, medical tourism serves as a vital catalyst for technological acquisition and, perhaps most importantly, as a primary defense against the "brain drain" of our most gifted medical professionals. By integrating private excellence with public duty, Tunisia is building a resilient ecosystem that translates foreign currency into local social impact.

2. The Economic Impact: A Pillar of National Growth

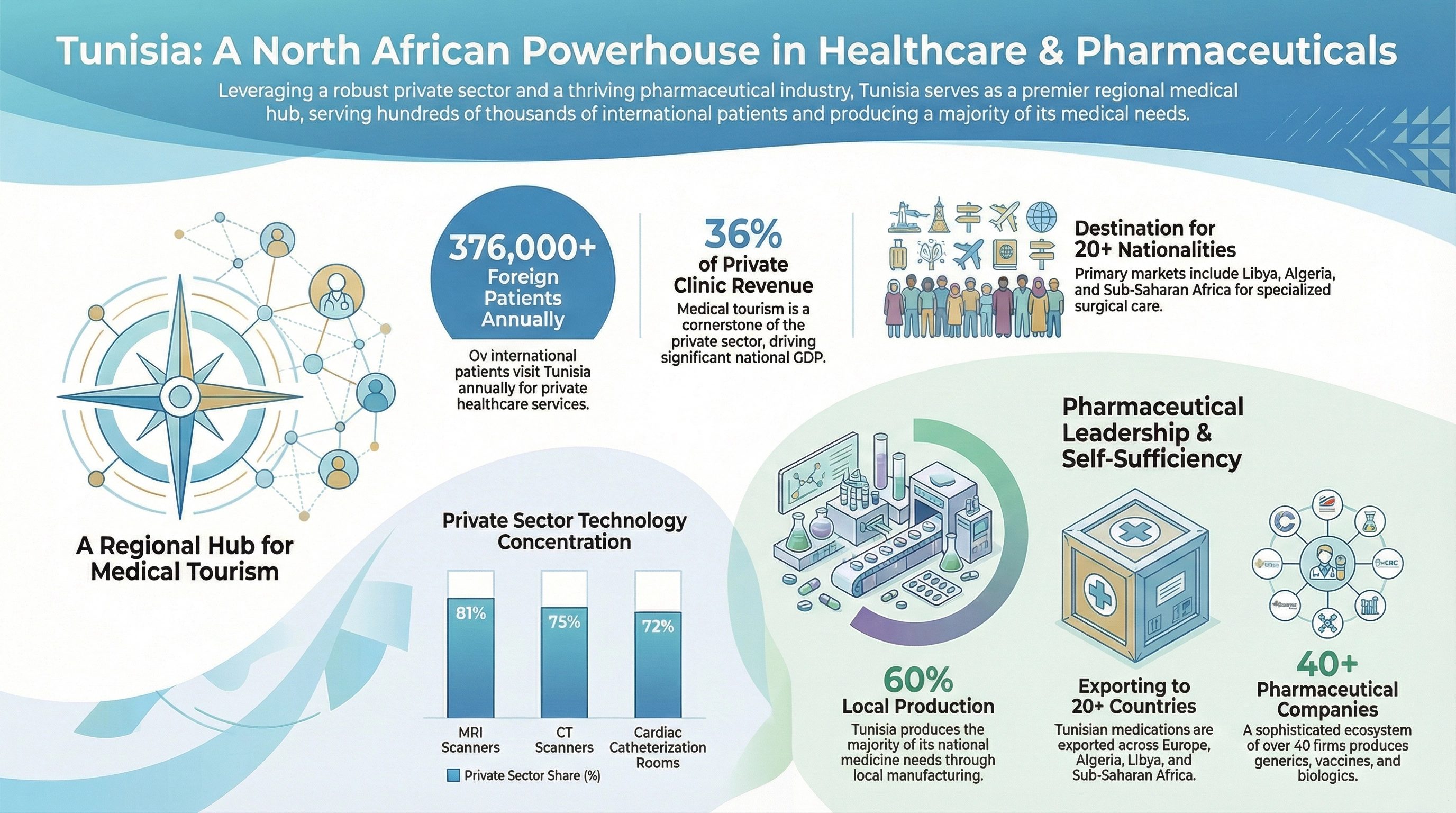

The economic weight of health services in Tunisia is substantial, though it faces a critical transition period. Historically, the sector has been heavily reliant on the "Libyan Factor," with Libyan patients once accounting for 84% of all foreign admissions. Recent strategic shifts have focused on diversifying this market toward Sub-Saharan Africa and European niche markets in dental care and cosmetic surgery.

3. Fighting the "Brain Drain": Retaining Tunisian Excellence

Tunisia’s healthcare system operates within a complex "Push vs. Pull" dynamic. The "Push" factors—economic uncertainty and deteriorating conditions in public hospitals—often drive elite talent toward Europe and the Gulf. However, the medical tourism boom provides a powerful "Pull" factor that keeps specialists on Tunisian soil.

A cornerstone of this retention strategy is the Complementary Private Activity (CPA) system, regulated by Decree No. 95-1634. This "Dual Practice" framework allows public sector professors and specialists to practice part-time in private clinics.

The Analyst’s View: While CPA allows top-tier experts to supplement their income and remain in the country to train the next generation, it is a double-edged sword. As an analyst, one must acknowledge the "Two-Tier" risk: the conflict of interest where private profitability can lead to absenteeism in public hospitals and the diversion of patients to the private sector. The 2030 Vision aims to refine this balance to ensure public sector duty remains paramount.

4. Technological Subsidization: Advanced Care for All

Medical tourism allows Tunisia to house medical technology that the local public sector alone could not afford. The high volume of international patients justifies the investment in "heavy equipment," which is subsequently made accessible to Tunisian citizens through the National Health Insurance Fund (CNAM) and strict accreditation standards set by INEAS.

Concentration of High-Tech Medical Equipment

| Equipment Type | Private Sector Share |

|---|---|

| CT Scanners | 75% |

| MRI Scanners | 81% |

| Cardiac Catheterization Rooms | 72% |

The Regional Challenge: Despite this concentration, a "shadow" of inequality persists. Governorates such as Tozeur and Kebili currently possess zero MRI scanners. The next frontier for investment must bridge the gap between the affluent coastal clusters (Tunis, Sousse, Sfax) and the underserved interior to achieve true universal equity.

5. A Robust Pharmaceutical Ecosystem: 60% Self-Sufficiency

Tunisia’s pharmaceutical sector is a pillar of national sovereignty, ensuring that the healthcare revolution is supported by a reliable domestic supply chain.

- Domestic Manufacturing: Local production meets 60% of national medicine needs, though the industry remains strategically focused on reducing its dependence on imported Active Pharmaceutical Ingredients (APIs).

- Market Leadership: Over 40 companies drive the sector, including pioneers like SIPHAT, Teriak, and Unimed, alongside major players Adwya and Medis Laboratories.

- Export Footprint: Tunisia currently exports medications to over 20 countries, leveraging Good Manufacturing Practices (GMP) to compete in European and Sub-Saharan African markets.

6. The Strength of the Tunisian Health System: By the Numbers

Tunisia’s healthcare performance is grounded in legislative frameworks and a commitment to social safety nets.

- Constitutional Mandate: Article 43 of the 2022 Constitution explicitly recognizes the right to health, mandating the State to guarantee quality care and universal coverage.

- Universal Insurance: Under Law No. 2004-71, the National Health Insurance Fund (CNAM) was unified. Today, over 4 in 5 Tunisians are covered by either CNAM or Free Medical Assistance (AMG).

- Epidemiological Success: Tunisia has achieved the near-eradication of measles, polio, and neonatal tetanus, shifting focus now toward non-communicable diseases (NCDs).

- Infrastructure Expansion: Based on 2018 data, 102 private clinics are operational, with an additional 87 clinics currently under construction or extension, set to add 6,500 beds to the national capacity.

7. Conclusion: Towards a 2030 Vision

The trajectory of Tunisian healthcare is codified in the National Health Policy 2030, the result of a decade-long "Societal Dialogue" that provides the system with democratic legitimacy. Tunisia’s path forward lies in evolving beyond a "two-tier" system toward a model of integrated public-private partnership (PPP). By leveraging the revenue of medical tourism to fund regional development and pharmaceutical innovation, Tunisia is not merely treating patients—it is engineering a resilient, world-class health economy.

8. Supporting References & Further Reading

- UNICEF: Tunisia Community Health Policy Landscape 2024

- WHO: Understanding the Private Health Sector in Tunisia (2024)

- African Development Bank: Health Services Export Strategy - Tunisia

- Carthage Magazine: Tunisia’s Pharma Sector Growth